All Categories

Featured

Table of Contents

Removing representative compensation on indexed annuities permits for considerably higher detailed and real cap rates (though still substantially reduced than the cap prices for IUL plans), and no question a no-commission IUL policy would certainly push illustrated and real cap prices higher also. As an aside, it is still possible to have a contract that is very rich in agent payment have high early cash surrender worths.

I will certainly concede that it goes to the very least theoretically POSSIBLE that there is an IUL plan out there issued 15 or twenty years ago that has actually supplied returns that are superior to WL or UL returns (more on this below), yet it's important to better recognize what a suitable comparison would certainly involve.

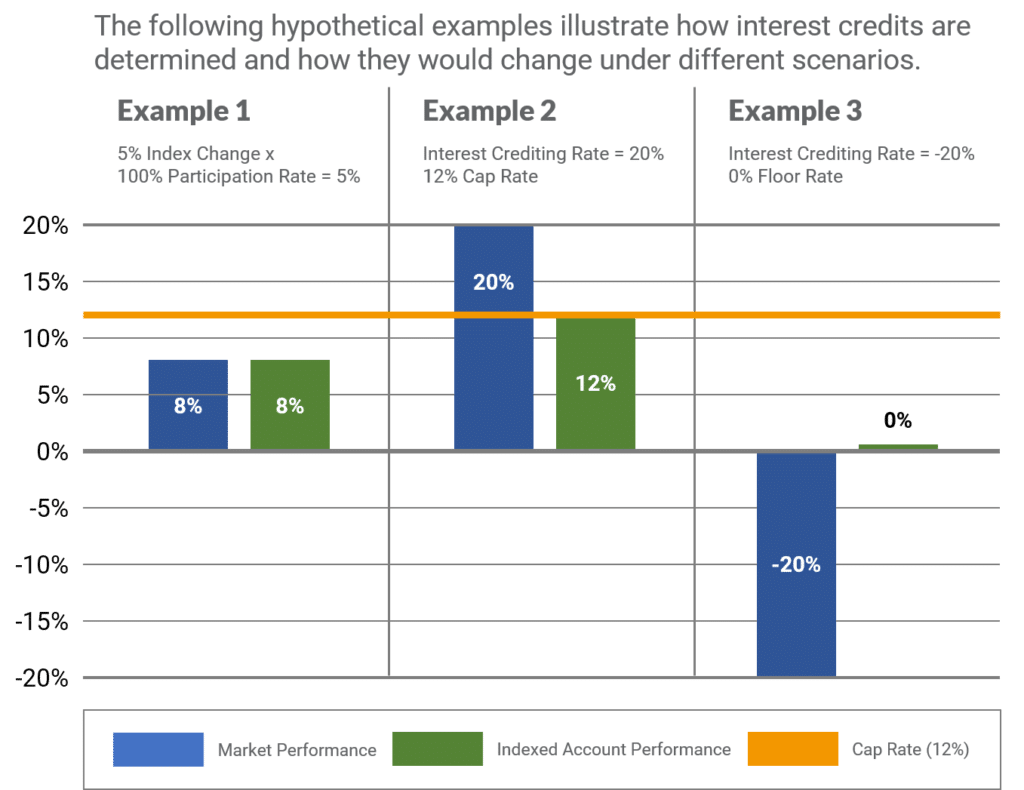

These policies commonly have one bar that can be evaluated the firm's discretion every year either there is a cap rate that specifies the optimum crediting price in that particular year or there is an involvement rate that specifies what percentage of any type of favorable gain in the index will be passed along to the plan in that particular year.

And while I normally concur with that characterization based on the auto mechanics of the plan, where I take problem with IUL proponents is when they characterize IUL as having remarkable returns to WL - fixed index universal life insurance pros and cons. Many IUL advocates take it an action further and factor to "historic" data that seems to support their claims

There are IUL policies in existence that carry even more danger, and based on risk/reward principles, those policies should have higher expected and actual returns. (Whether they in fact do is a matter for serious dispute however firms are using this method to help warrant greater detailed returns.) Some IUL plans "double down" on the hedging strategy and analyze an extra cost on the plan each year; this fee is after that made use of to enhance the alternatives spending plan; and then in a year when there is a favorable market return, the returns are enhanced.

Indexed Insurance Policy

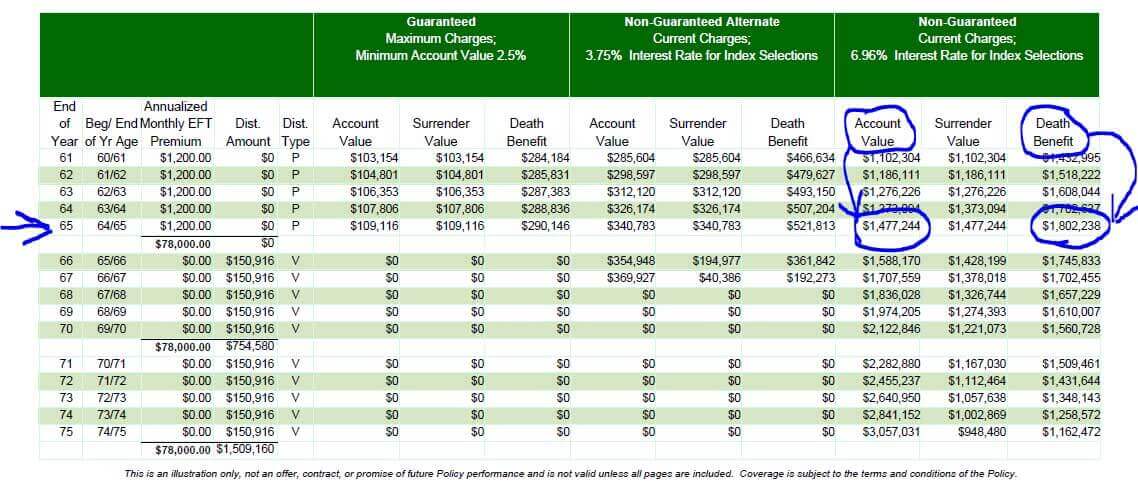

Consider this: It is possible (and as a matter of fact likely) for an IUL plan that averages a credited price of say 6% over its initial ten years to still have a total adverse price of return during that time as a result of high fees. Lots of times, I locate that agents or consumers that brag about the efficiency of their IUL plans are puzzling the credited price of return with a return that correctly shows all of the plan charges.

Next we have Manny's question. He claims, "My good friend has actually been pushing me to get index life insurance and to join her company. It looks like a Multi level marketing.

Insurance coverage sales people are tolerable individuals. I'm not suggesting that you 'd dislike yourself if you claimed that. I said I made use of to do it? That's just how I have some understanding. I used to market insurance coverage at the start of my profession. When they offer a costs, it's not unusual for the insurance company to pay them 50%, 80%, also in some cases as high as 100% of your first-year costs.

It's hard to market because you obtained ta constantly be looking for the next sale and going to locate the next individual. It's going to be difficult to find a whole lot of gratification in that.

Let's speak about equity index annuities. These things are prominent whenever the markets remain in an unstable duration. But below's the catch on these points. There's, initially, they can control your habits. You'll have abandonment durations, normally 7, 10 years, perhaps even past that. If you can't get accessibility to your money, I understand they'll inform you you can take a small percentage.

Nationwide Yourlife Indexed Ul Accumulator

Their abandonment durations are big. That's exactly how they understand they can take your money and go totally invested, and it will be alright since you can't obtain back to your money until, once you're right into 7, 10 years in the future. That's a lengthy term. Regardless of what volatility is going on, they're possibly mosting likely to be great from an efficiency viewpoint.

There is no one-size-fits-all when it comes to life insurance. Getting your life insurance plan best takes into account a variety of elements. [video description: Pleasant music plays as Mark Zagurski speaks to the camera.] In your busy life, financial freedom can look like an impossible goal. And retirement might not be leading of mind, due to the fact that it appears so much away.

Pension plan, social security, and whatever they 'd handled to conserve. It's not that easy today. Fewer companies are offering standard pension plan strategies and lots of firms have actually reduced or terminated their retirement and your ability to depend only on social protection is in question. Even if advantages haven't been reduced by the time you retire, social safety and security alone was never ever meant to be adequate to spend for the lifestyle you desire and are entitled to.

Guaranteed Universal Life Insurance Rates

/ wp-end-tag > As part of an audio economic approach, an indexed global life insurance policy can help

you take on whatever the future brings. Before committing to indexed universal life insurance policy, here are some pros and disadvantages to consider. If you pick a good indexed universal life insurance plan, you might see your cash value grow in worth.

Given that indexed global life insurance coverage needs a specific level of threat, insurance policy business often tend to maintain 6. This kind of strategy likewise supplies.

Normally, the insurance business has a vested rate of interest in doing much better than the index11. These are all aspects to be considered when selecting the best kind of life insurance coverage for you.

Given that this kind of plan is a lot more complex and has a financial investment element, it can commonly come with greater costs than other policies like whole life or term life insurance coverage. If you don't believe indexed universal life insurance policy is appropriate for you, right here are some choices to take into consideration: Term life insurance policy is a temporary policy that commonly supplies coverage for 10 to thirty years.

National Life Iul

When determining whether indexed universal life insurance policy is ideal for you, it is necessary to take into consideration all your options. Whole life insurance policy may be a much better option if you are looking for more stability and consistency. On the various other hand, term life insurance policy may be a much better fit if you just require insurance coverage for a particular amount of time. Indexed universal life insurance policy is a kind of plan that provides a lot more control and flexibility, together with greater cash money worth growth possibility. While we do not offer indexed global life insurance, we can supply you with even more details concerning entire and term life insurance coverage plans. We advise exploring all your choices and talking with an Aflac agent to find the most effective fit for you and your family members.

The rest is included to the money worth of the policy after fees are deducted. While IUL insurance policy might prove beneficial to some, it's important to recognize exactly how it functions before buying a policy.

{kind=link}

Latest Posts

Life Insurance Surrender Cost Index

Equity Indexed Insurance

Guaranteed Universal Life Quotes